The United Arab Emirates (UAE) offers foreign investors several business opportunities, including providing some companies with a 0% Corporate Tax (CT) on qualifying income under certain conditions. The Corporate Tax in the UAE is set by the Federal Tax Authority (FTA), the governing authority of tax in the UAE.

The Corporate Tax Law shall apply to tax periods commencing on or after June 1, 2023. Corporate tax is imposed on taxable income at the following rates:

- 0% (zero percent) on the portion of the taxable income not exceeding AED 375,000

- 9% (nine percent) on the portion of the taxable income exceeding AED 375,000

While the above rates are generic, specific rates are mentioned for the free zones as below:

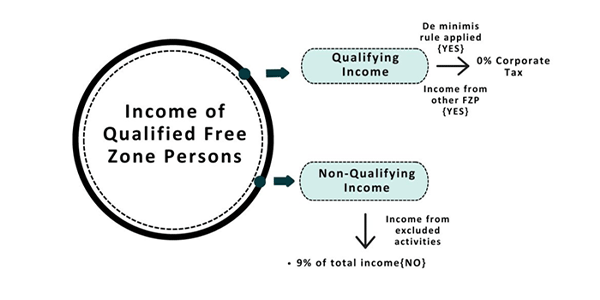

- 0% corporate tax rate on its qualifying income

- 9% on its non-qualifying income

It is to be noted that the tax incentives provided by the respective free zones would still be valid as long as businesses meet the compliance requirements. It is also necessary that they do not conduct business with the UAE mainland companies or individuals, except within the de-minimis levels. The blog provides information on all details applicable to the free zones including definition of qualifying free zone and qualifying income.

A free zone person is defined as a juridical person incorporated, established, or otherwise registered in a free zone, including a branch of a non-resident person registered in a free zone. However, to be considered a qualifying free zone person, the following additional requirements are to be met:

- Derive qualifying income

- Maintain adequate substance in the UAE

- Satisfy the de minimis requirement

- Have not elected to be subject to Corporate Tax

- Comply with the transfer pricing rules and documentation requirements under the Corporate Tax law

- Prepare and maintain audited financial statements for the Corporate Tax Law

The Minister may prescribe additional conditions to be met by a free zone person to be considered as a Qualifying Free Zone Person.

1. What Is Qualifying Income?

- Income from transactions with other free zone persons except for income derived from excluded activities

- Income from transactions with any Non-Free Zone Person, domestic and foreign, only in the case of qualifying activities that are not excluded activities

- Any other income where the de minimis requirement is satisfied

It should be noted that Qualifying Free Zone Persons are not entitled to a 0% rate on their first AED 375,000 of non-qualifying Income. They will be rather taxed at the general rate of 9%.

2. What Are Excluded Activities in the Context of Qualifying Income for Free Zones?

The Excluded Activities are the transactions with natural persons, except for certain Qualifying Activities. Excluded Activities include:

- Banking, insurance, finance, and leasing activities except for certain exceptions

- Ownership or exploitation of the UAE immovable property, other than Commercial Property located in a free zone provided such activity to immovable property located in a free zone is conducted with other free zone persons

- Ownership or exploitation of intellectual property assets

- Ancillary Activities (which serve no independent function) to the above activities

3. What Are Qualifying Activities?

Qualifying Income includes income derived from transactions with Non-Free Zone Persons only in respect of Qualifying Activities. They include:

- Manufacturing of goods or materials

- Processing of goods or materials

- Holding of shares and other securities

- Ownership, management, and operation of ships

- Reinsurance services subject to the regulatory oversight of the relevant competent authority in the UAE

- Fund management services subject to regulatory oversight by the relevant competent authority in the UAE

- Wealth and investment management services subject to regulatory oversight by the relevant competent authority in the UAE

- Headquarters services to related parties

- Treasury and financing services to related parties

- Financing and leasing of Aircraft, including engines and rotatable components

- Distribution of goods or materials in or from a Designated Zone to a customer that resells such goods or materials, or parts thereof, or processes or alters such goods or materials or parts thereof for sale or resale

- Logistics services

- Any ancillary activities (which serve no independent function) to the above activities

4. What Are Adequate Substance Requirements?

A Qualifying Free Zone Person (QFZP) shall undertake its core income-generating activities in a free zone and, having regard to the level of the activities carried out, have adequate assets, an adequate number of qualified employees, and incur an adequate number of operating expenditures.

Activities can be outsourced to a related party in a free zone or a third party in a free zone, provided the Qualifying Free Zone Person has adequate supervision of the outsourced activity.

5. What Is the De Minimis Requirement?

The de minimis requirements are met where the non-qualifying revenue in a tax period does not exceed:

- AED 5,000,000

- 5% of total Revenue (calculated as the total amount of non-qualifying revenue/total revenue)

The de minimis requirement allows a Qualifying Free Zone Person to earn a small or incidental amount of non-qualifying Income without being disqualified from the free zone corporate tax regime.

While the Qualifying Free Zone Person status looks tax attractive, there are certain disadvantages. They are as follows:

- Tax losses cannot be transferred between taxable resident judicial persons

- It cannot form part of a tax group

- No business restructuring relief will be available

- No small business relief can be claimed