The Importance of Tax Registration in the UAE

Businesses in the United Arab Emirates (UAE), local or international, multinational or small to medium-sized, must comply with the UAE tax legislation and register with the applicable tax authorities when they meet the requirements. Gatestone Group Tax Registration Services in the UAE ensure that businesses are not just compliant but also primed for success in the UAE.

THE IMPORTANT FACTORS OF TAX REGISTRATION SERVICES IN THE UAE

- Taxes applicable in the UAE

While the UAE offers tax advantages, it is crucial to identify the taxes applicable to your UAE business based on applicable provisions.

- Mandatory tax registration thresholds

There are clear revenue thresholds that, when met, mandate tax registration. Missing these can result in penalties.

- Voluntary tax registration benefits

Even if not mandated, voluntary registration benefits businesses in the UAE marketplace.

Taxes Applicable in the UAE

The types of taxes applicable in the UAE include:

Corporate Tax (CT)

The Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses (“Corporate Tax Law”) was signed on October 3, 2022. The provisions of the Corporate Tax Law shall apply to tax periods commencing on or after June 1, 2023. Generally, Corporate Tax in the UAE is imposed at a rate of 9% on taxable income exceeding AED 375,000.

Value Added Tax (VAT)

Federal Decree-Law No. 8 of 2017 deals with the provisions on VAT in the UAE and came into effect as of January 1, 2018. The VAT rate in the UAE is 5% and is applicable to goods and services that are bought and sold. Businesses are responsible for collecting and paying VAT to the Federal Tax Authority (FTA).

Excise tax

An excise tax is levied on certain goods that are considered to be harmful to the environment or human health, such as electronic cigarettes, tobacco products, carbonated drinks, etc. The excise tax rates vary depending on the product.

Customs duties

A customs duty of 5% is generally imposed on the cost, insurance, and freight (CIF) value of imports. However, there are several exemptions and reliefs available, and certain goods, such as alcohol and tobacco, are subject to higher rates of duty.

Property Taxes

Property tax is levied on the value of real estate property in the UAE. The property tax rates could differ between Emirates.

Tourism Taxes

Tourism tax is levied on hotel stays and other tourist activities, and tax rates could differ between Emirates.

Here is a table summarising the main taxes in the UAE:

|

Tax |

Rate |

|

Corporate Tax (CT) |

9% |

|

Value Added Tax (VAT) |

5% |

|

Excise tax |

Varies |

|

Customs duties |

Generally 5%, but higher rates apply to certain goods |

|

Property taxes |

Varies by Emirate |

|

Tourism taxes |

Varies by Emirate |

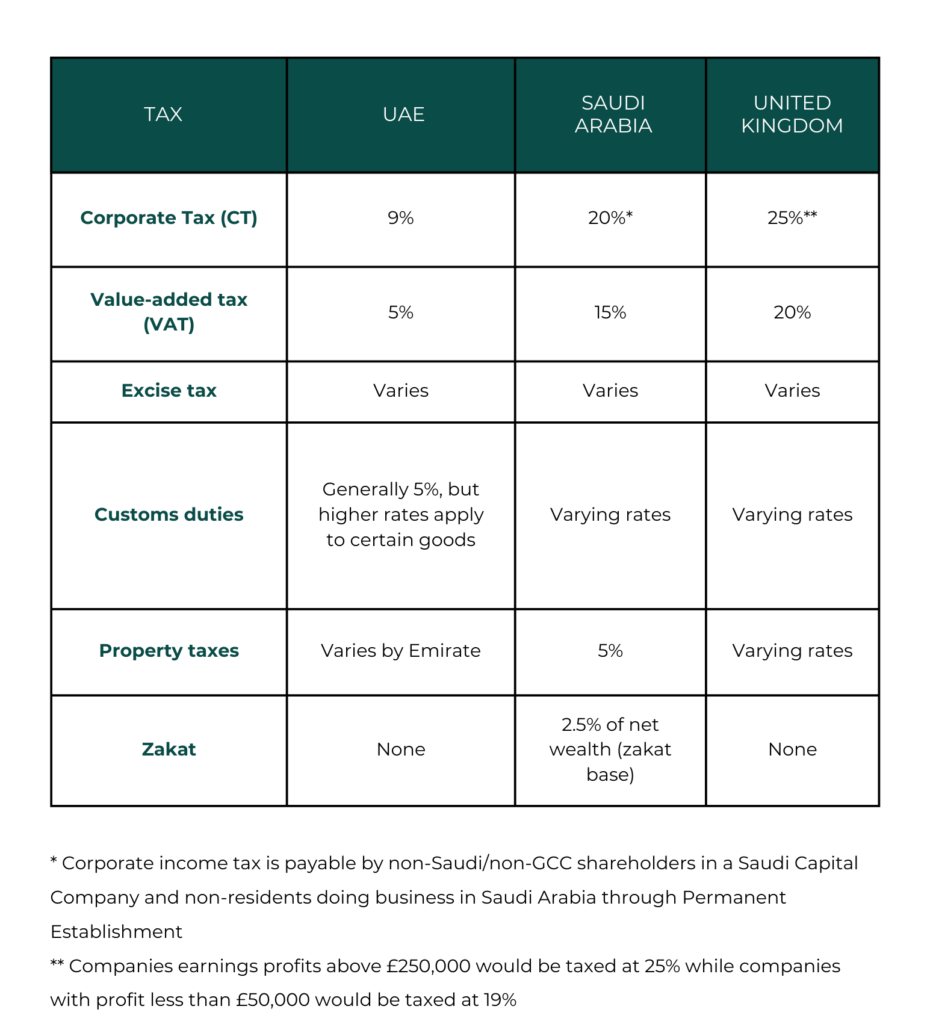

Tax categories and rates in the UAE, Saudi Arabia, and the United Kingdom

VAT in the UAE

Who should register under Value Added Tax in the UAE?

All UAE businesses must register for VAT if the value of their taxable supplies and imports in the past 12 months exceeded or is expected to exceed in the next 30 days beyond the AED 375,000 mandatory tax registration threshold.

A UAE business may choose to register for VAT voluntarily if their supplies or imports are less than the mandatory tax registration but exceed the voluntary threshold of AED 187,500.

Who is exempt from VAT in the UAE?

VAT in the UAE applies at a rate of 5%, except in the below-mentioned zero-rated and exempt categories:

Zero-rated sectors: VAT will be charged at 0% with respect to the following main categories of supplies:

- Supplies of certain sea, air, and land means of transportation (such as aircraft and ships)

- Certain investment-grade precious metals (e.g., gold and silver, of 99% purity or more)

- A direct or indirect export of goods to outside the Implementing States as specified in the Executive Regulation of this Decree-Law International transport of passengers and goods that starts or ends in the State or passes through its territory, including transport-related services

- Newly constructed residential properties that are supplied for the first time within three years of their construction

- Supply of certain education and healthcare services, and supply of relevant goods and services

VAT-exempt sectors

- Bare land

- Local passenger transport

- Supply of residential buildings through sale or lease, other than that which is zero-rated according to Clauses (9) and (11) of Article (45) of this Decree-Law

- Residential properties

Documents required for VAT registration

The UAE VAT registration system requires the submission of necessary documentation. Businesses must provide the following documents for the registration process:

- Business Trade License or Commercial License

- Passport copies and Emirates ID of the owner or partners, as mentioned on the license

- Memorandum of Association (MOA)

- Complete company address

- Contact details of the authorised signatory, including email and phone number

- Company bank details

- Details of any branches, if applicable

- Turnover declaration for the last 12 months, signed and stamped by the owner of the company and printed on the company’s letterhead

- Sample of sales or purchase invoices (signed and stamped)

- Expected revenue, turnover, and taxable expenses for the next 30 days

- Custom code along with a copy of the Dubai Customs letter, if applicable.

- Preference for registration as a tax group

Additional documents may be required based on the business activity and jurisdiction of the business.

Corporate Tax in the UAE

The Federal Decree-Law No. 47, also known as the Corporate Tax Law, was issued on October 10, 2022, and laid out the legal framework and guidelines for the implementation of the UAE Corporate Tax. The provisions of the Corporate Tax Law shall apply to tax periods commencing on or after June 1, 2023.

The corporate tax in the UAE is implemented at a rate of 9% for businesses operating in the UAE. It will be calculated based on taxable profits greater than the minimum threshold of AED 375,000, thus not affecting many small businesses.

Who should register under the UAE Corporate Tax?

The Federal Tax Authority (FTA) requires every taxable person to register with the UAE Corporate Tax based on the prescribed timeline and obtain a Tax Registration Number (TRN). The UAE Corporate Tax shall be applied to the taxable income of businesses at the following rates:

- 0% corporate tax rate for taxable income up to AED 375,000

- 9% corporate tax rate for taxable income greater than AED 375,000

Documents required for UAE corporate tax registration

Corporate tax registration in the UAE requires the submission of necessary documentation. Businesses must provide the following documents for the registration process:

- Business Trade License or Commercial License

- Passport copies and Emirates ID of the owner or partners, as mentioned on the license

- Memorandum of Association (MOA)

- Article of Association (AOA)

- The concerned person’s contact details

- Company address and P.O. Box

- Financial Year-end

- If there is more than one partner, the partners’ details and percentage of interest

Who is subject to UAE Corporate Tax?

The Corporate Tax in the UAE applies to local and foreign-owned companies in the UAE that are managed and controlled in the UAE.

If a natural person conducts business in the UAE directly, through an unincorporated partnership, or as a sole proprietorship, they will be liable for the UAE Corporate Tax.

How is taxable income determined for the UAE Corporate Tax?

Based on the Corporate Tax Law, the taxable income for a tax period will be the accounting net profit (or loss) of the business once the adjustments for certain items have been made.

The accounting net profit (or loss) of the company, after deducting certain items listed in the Corporate Tax Law and associated implementing decisions, will be the taxable income for a given tax period.

A company’s accounting net profit (or loss) is the amount shown in its International Financial Reporting Standards (IFRS)-compliant financial statements.

The accounting net profit (or loss) will require the following items to be adjusted:

- Unrealised gains and losses (subject to the election made regarding the application of the realisation principle)

- Exempt income, such as qualifying dividends and capital gains

- Deductions that are not allowable for Corporate Tax purposes

- Reliefs for specific transaction types

- Transfer pricing adjustments relating to transactions between related parties or connected persons

- Tax Losses

- Gains or losses arising on transfers within a qualifying group

- Gains or losses arising from transfers arising from qualifying business restructuring transactions

- Any other adjustments as specified by the Minister

Does the free zone Corporate Tax regime apply to a foreign company in the UAE?

Yes, a foreign company can benefit from the free zone Corporate Tax regime based on its Qualifying Income.

What income is exempt from UAE Corporate Tax?

The income listed below is not subject to UAE Corporate Tax:

- Dividends and other profit distributions from UAE-based entities

- Dividends and other profit distributions from a participating interest in a foreign entity

- Additional income types (e.g., capital gains, forex transactions, impairment gains and losses) from participating interests

- Income from a foreign permanent establishment

- Income earned by non-residents from aircraft or ship operations or leasing in international transportation (subject to specific conditions)

Who will be required to register for the UAE Corporate Tax?

All legal entities in the UAE will be required to register for the UAE Corporate Tax and obtain a Corporate Tax registration Number.

How are non-residents subject to the UAE Corporate Tax?

For non-residents, the Corporate Tax in the UAE is only applicable to two types of income:

- Income from their Permanent Establishment in the UAE: If you have a business presence or establishment within the UAE, Corporate Tax may apply to the income generated from that establishment.

- Income sourced in the UAE: Non-residents may be subject to the UAE Corporate Tax on income sourced within the UAE. However, it’s important to note that this income is currently subject to a 0% withholding tax.

Who is exempt from Corporate Tax in the UAE?

The UAE Corporate Tax is exempt from certain types of business or business activity. They are known as exempt persons and include the following:

Automatically exempt:

- Government entities

Exempt if notified to the Ministry of Finance (and subject to meeting certain conditions):

- Extractive businesses

- Non-extractive natural resource businesses

Exempt if listed in a cabinet decision:

- Government-controlled entities and Qualifying public benefit entities

Exempt if applied to and approved by the Federal Tax Authority (and subject to meeting certain conditions):

- Public or private pensions and social security funds

- Qualifying investment funds

- Juridical persons incorporated in the UAE that are wholly owned and controlled by certain exempt persons

- Any other person as may be determined in a decision issued by the Cabinet at the suggestion of the Minister

Ensure Compliance with Gatestone Group

With the help of Gatestone group tax registration experts, stay compliant and ensure smooth execution of tax registration services in the UAE. Minimise the risks associated with the UAE taxes with careful preparation and navigate the UAE tax laws seamlessly with our consultants by your side.

FAQs

Voluntary registration can enhance business credibility, opening doors to specific markets and clientele.

We have a dedicated team of tax experts who monitor changes, ensuring our clients are always informed and updated.

We offer ongoing support, periodic reviews, and updates on changing regulations, ensuring businesses remain compliant.

The specific taxes depend on your business activities. Common taxes include Corporate Income Tax, VAT (Value Added Tax), and excise tax.

Yes, our services cover a range of tax return filings, including VAT, Corporate Tax, and any other applicable taxes, ensuring comprehensive business tax compliance.

Required documents vary but may include financial statements, invoices, receipts, and other financial records. Our tax experts will guide you through the specific documentation needed.

Non-compliance with tax filing in the UAE can result in financial penalties and legal consequences. Our services are designed to ensure your company meets all tax filing deadlines and requirements.

We are leading experts in company formation and business setup in the UAE.

Contacts

-

Office 1416, The Binary by Omniyat Marasi Drive Street, Business Bay, Dubai

-

+971 4 450 1023

+971 52 410 0849 -