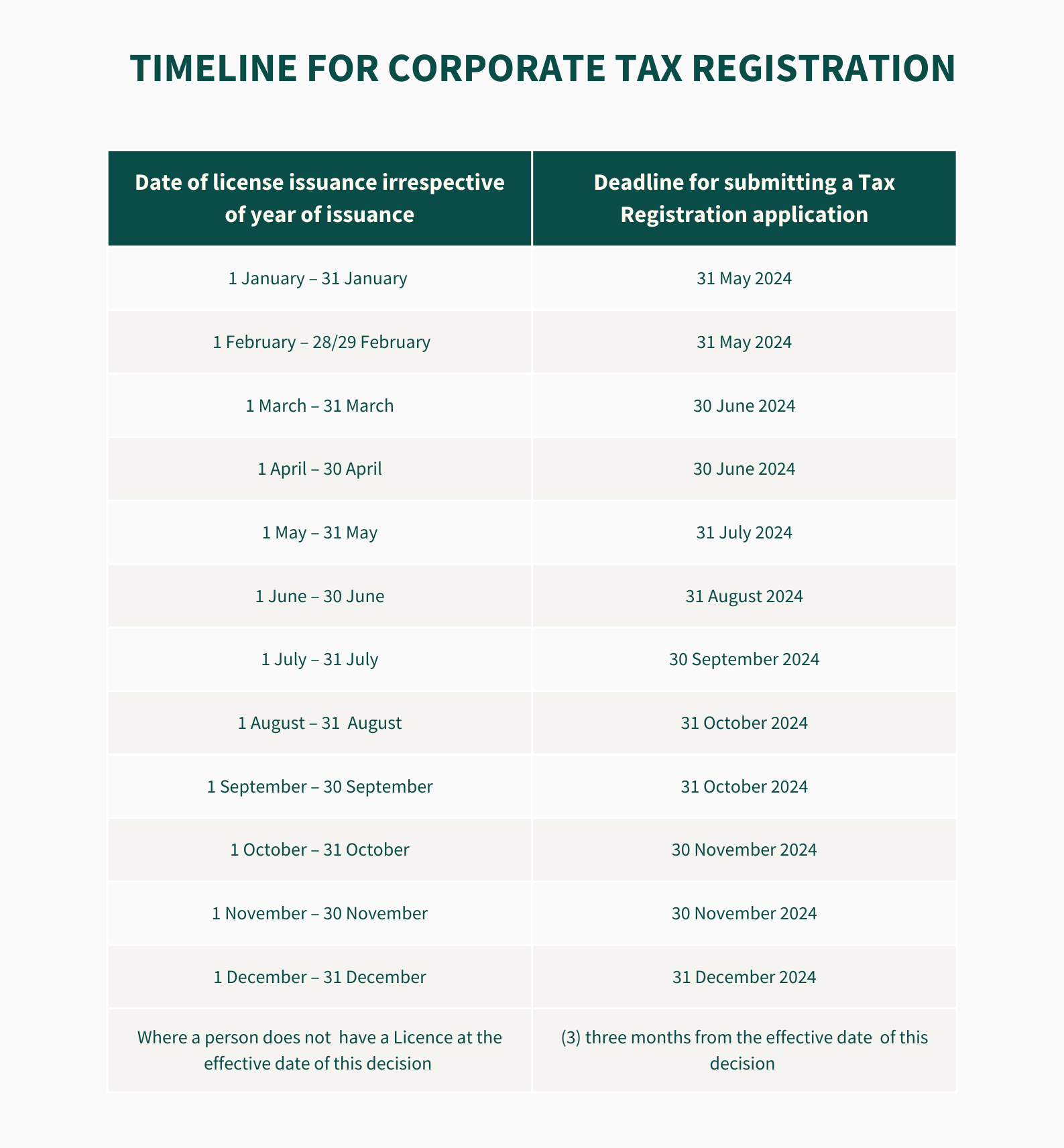

The FTA has recently announced the deadlines for corporate tax registration. Existing businesses must register within the timeline as below:

A few other points to consider include:

- New businesses must register within 3 months of incorporation. Late registration could result in a penalty of AED 10,000.

- Additionally, businesses must file the tax return and pay it within nine months following the completion of their financial year. Administrative penalties could be a result of late filing or payment.

- Taxable persons should maintain records and documentation that support the information provided in a tax return. These records and documents must be kept for seven years following the end of the tax period to which they relate.